What Is An ABA Number: A Comprehensive Guide To Understanding ABA Routing Numbers

ABA numbers play a crucial role in the banking system, ensuring seamless transfer of funds between financial institutions. If you’ve ever wondered what an ABA number is and why it’s essential, this article will provide you with a detailed explanation. Whether you’re setting up direct deposits, initiating wire transfers, or paying bills online, understanding ABA numbers can make all the difference.

In today's digital age, banking has become more convenient than ever. However, behind the scenes, there are complex systems that ensure your transactions are processed correctly. One such system involves the use of ABA numbers, which serve as the backbone of domestic transfers within the United States.

As we delve deeper into this topic, you’ll discover how ABA numbers function, their importance in banking operations, and how to locate them for your personal or business accounts. By the end of this article, you’ll have a thorough understanding of ABA numbers and their significance in financial transactions.

Read also:A Vintage Wonderland Step Back In Time To A Magical Era

Table of Contents

- What is an ABA Number?

- History and Evolution of ABA Numbers

- Structure and Components of an ABA Number

- Common Uses of ABA Numbers

- How to Find Your ABA Number

- ABA Numbers vs. SWIFT Codes

- Security Considerations for ABA Numbers

- Common Errors and Troubleshooting

- Regulations and Compliance

- The Future of ABA Numbers

What is an ABA Number?

An ABA number, also known as a routing transit number (RTN), is a nine-digit code assigned to financial institutions in the United States. This number serves as an identifier for banks and credit unions, enabling the routing of funds between institutions during transactions. The American Bankers Association (ABA) originally developed this system in 1910, hence the name "ABA number."

Key Features of ABA Numbers

- Unique to each financial institution

- Used for domestic transactions only

- Facilitates automatic clearing house (ACH) transactions

- Essential for direct deposits, bill payments, and wire transfers

ABA numbers ensure that funds are directed to the correct bank or credit union, streamlining the transaction process. Without these numbers, financial institutions would struggle to process payments efficiently.

History and Evolution of ABA Numbers

The concept of ABA numbers dates back to 1910 when the American Bankers Association introduced the routing transit number system. Initially designed to simplify check processing, the system has evolved to accommodate modern banking needs, including electronic transactions.

Key Milestones in ABA Number Development

- 1910: Introduction of the ABA routing transit number system

- 1950s: Adoption of magnetic ink character recognition (MICR) technology

- 1970s: Expansion to include electronic transactions

- Present day: Integration with digital banking platforms

As banking technology continues to advance, ABA numbers remain a vital component of the financial infrastructure, adapting to meet the demands of an increasingly digital world.

Read also:Treadmill Yzy The Ultimate Fitness Revolution

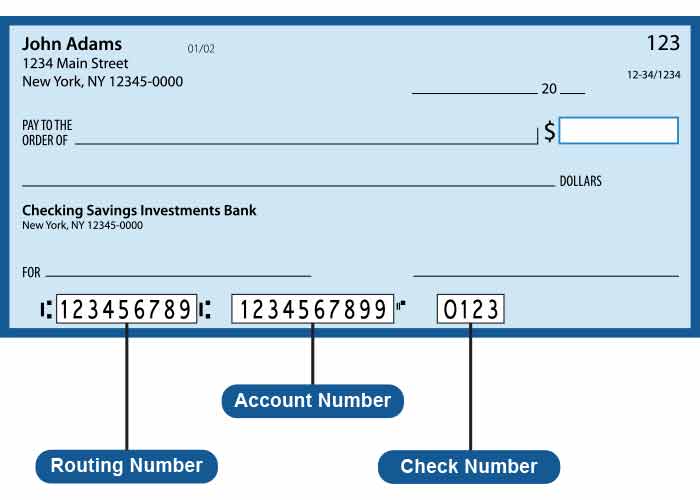

Structure and Components of an ABA Number

An ABA number consists of nine digits, each serving a specific purpose. Understanding the structure of an ABA number can help you identify potential errors and ensure accurate transaction processing.

Breaking Down the ABA Number

- First four digits: Identify the Federal Reserve Bank district and branch

- Fifth and sixth digits: Represent the bank’s location within the district

- Seventh digit: Indicates the type of institution (e.g., commercial bank, savings bank)

- Last two digits: Serve as a checksum to verify the accuracy of the number

By understanding the components of an ABA number, you can better appreciate its role in facilitating secure and efficient financial transactions.

Common Uses of ABA Numbers

ABA numbers are integral to various banking activities, ensuring seamless processing of transactions. Below are some of the most common uses of ABA numbers:

- Direct deposits: Automating salary payments and government benefits

- Bill payments: Facilitating online and automatic payments to vendors

- Wire transfers: Transferring funds between accounts at different institutions

- ACH transactions: Processing electronic payments and transfers

Whether you’re setting up recurring payments or transferring money to a friend, ABA numbers ensure that your transactions are processed accurately and securely.

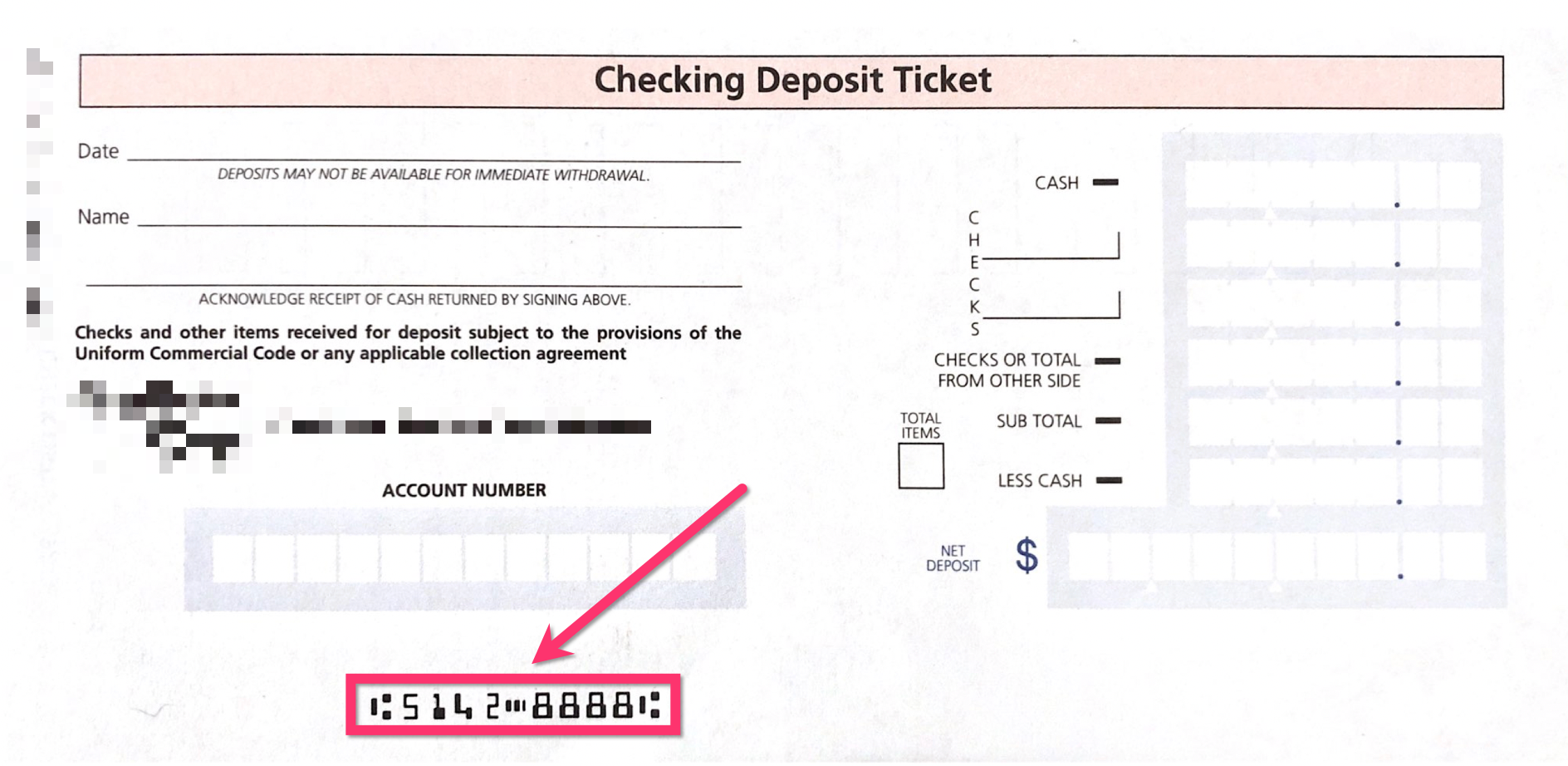

How to Find Your ABA Number

Locating your ABA number is a straightforward process. Here are several methods to help you find it:

Method 1: Check Your Checks

On the bottom left corner of your checks, you’ll find a series of numbers. The first set of nine digits represents your ABA number.

Method 2: Online Banking

Most banks provide ABA numbers through their online banking platforms. Simply log in to your account and navigate to the account information section.

Method 3: Contact Your Bank

If you’re unable to locate your ABA number through the above methods, contact your bank’s customer service department for assistance.

Regardless of the method you choose, ensuring you have the correct ABA number is crucial for successful transaction processing.

ABA Numbers vs. SWIFT Codes

While ABA numbers and SWIFT codes both facilitate financial transactions, they serve different purposes and operate within distinct systems. ABA numbers are used exclusively for domestic transactions within the United States, whereas SWIFT codes enable international transfers.

Key Differences Between ABA Numbers and SWIFT Codes

- Scope: ABA numbers for domestic use; SWIFT codes for international use

- Format: ABA numbers are nine digits; SWIFT codes are alphanumeric and up to 11 characters

- Functionality: ABA numbers for ACH transactions; SWIFT codes for wire transfers

Understanding the distinction between these two systems can help you choose the appropriate code for your transaction needs.

Security Considerations for ABA Numbers

While ABA numbers are essential for financial transactions, they must be handled with care to prevent unauthorized access and potential fraud. Below are some security tips to protect your ABA number:

- Keep your ABA number confidential and share it only when necessary

- Monitor your accounts regularly for unauthorized transactions

- Use secure methods for transmitting ABA numbers, such as encrypted email or secure messaging platforms

By following these security practices, you can minimize the risk of fraud and ensure the safety of your financial information.

Common Errors and Troubleshooting

Mistakes in ABA numbers can lead to transaction failures or delays. Here are some common errors and how to address them:

- Transposing digits: Double-check the ABA number to ensure accuracy

- Using outdated numbers: Verify the ABA number with your bank before initiating a transaction

- Incorrect institution: Confirm that the ABA number corresponds to the correct bank or credit union

If you encounter issues with your transaction, contact your bank’s customer service department for assistance in resolving the problem.

Regulations and Compliance

ABA numbers are subject to various regulations and compliance standards to ensure their proper use and security. The Federal Reserve and other regulatory bodies oversee the ABA number system, ensuring that financial institutions adhere to established guidelines.

Key Regulations Affecting ABA Numbers

- Electronic Fund Transfer Act (EFTA): Protects consumers during electronic transactions

- Gramm-Leach-Bliley Act (GLBA): Requires financial institutions to safeguard sensitive customer information

- Bank Secrecy Act (BSA): Mandates reporting and record-keeping for financial transactions

By adhering to these regulations, financial institutions help maintain the integrity and security of the ABA number system.

The Future of ABA Numbers

As technology continues to evolve, the role of ABA numbers in the financial system may change. Innovations such as real-time payment systems and blockchain technology could transform how transactions are processed, potentially reducing the reliance on traditional ABA numbers.

However, for the foreseeable future, ABA numbers will remain a critical component of the banking infrastructure, ensuring efficient and secure transaction processing. Financial institutions and regulators will continue to adapt to new technologies, ensuring that ABA numbers remain relevant in an ever-changing landscape.

Conclusion

In summary, ABA numbers are essential for facilitating domestic financial transactions in the United States. By understanding their structure, uses, and security considerations, you can ensure accurate and secure processing of your transactions. Whether you’re setting up direct deposits, initiating wire transfers, or paying bills online, ABA numbers play a vital role in the banking system.

We encourage you to share this article with others who may benefit from understanding ABA numbers. Additionally, feel free to leave a comment or question below, and don’t hesitate to explore other informative articles on our site. Together, let’s enhance our knowledge of the financial world and stay ahead in the digital age.

{kind=link}